The Maldives experienced the worst economic downturn in recorded history in 2020 as a result of the Covid-19 pandemic, with real GDP (Gross Domestic Product) declining by 33.5 percent (Figure 1). The impact of the disruption to international travel and domestic economic activity was felt acutely not just by households and businesses, but by the government as well.

Government revenue realization in 2020 was about half of what was initially forecasted in the budget, and 34 percent lower compared to the revenue realized in 2019. Despite the government reducing expenditure by 20 percent during the year compared to budgeted levels, the dominating impact of the revenue crunch resulted in an overall fiscal deficit of 23 percent of GDP, up from the budgeted deficit of 6.2 percent of GDP.

Saving lives and livelihoods was the government’s priority at this time of crisis. The decision to finance the deficit by issuing debt while maintaining support to the health sector, households and businesses was one taken knowingly, for the alternative of not doing this on account of fiscal consolidation was unacceptable. Economist Barry Eichengreen and co-authors succinctly state this argument in their book “In Defense of Public Debt”: “Indeed, a government that did not borrow in order to provide essential services during a deadly pandemic- … -would be accused of dereliction, and rightly so. Such a government, to continue the analogy with a household, would be like parents who refused to borrow to obtain life-saving surgery for a child.”

The results of this decision have already been observed. The adequate health response made the Maldives one of the first countries to contain the spread of Covid-19. On the economic front, the country was among the five economies with the highest growth globally in both 2021 and 2022. Consequently, the economy recovered back to pre-pandemic levels by the end of 2022.

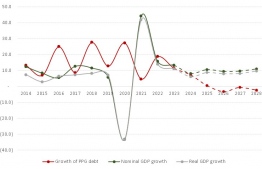

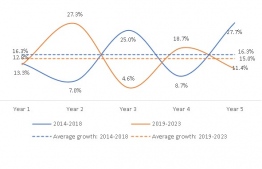

However, the cost of averting almost certain disaster in the face of the pandemic is an elevated debt level. In particular, the year 2020 saw public and publicly guaranteed (PPG) debt increase from 78.8 percent of GDP to 150.2 percent of GDP. But even with this large, and largely unavoidable, spike in the ratio, the average growth rate of public debt between 2019 and 2023, which is at 15 percent, is still lower compared to the average growth rate of public debt between 2014 and 2018, which stands at 16.3 percent (Figure 2).

The economic recovery has already led to a significant decline in the indicator, with public debt to GDP expected to decline to 110 percent by the end of this year. But the risks from the increase in debt will need to be addressed over the medium term through fiscal reform and prudent debt management. On debt management, the issuance of a sukuk at a single digit coupon rate in the first half of 2021 when global financial markets were in turmoil is proof enough that we are in good hands.

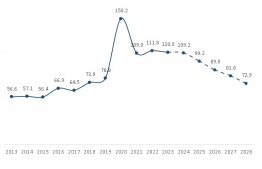

The oversubscription of the tap issuance on the sukuk later that year by over three times further demonstrated the confidence of investors in the Maldives. On the fiscal side, reforms are already underway to increase the tax base and increase the efficiency of expenditure. Fiscal reforms have been calibrated to reduce the deficit to levels than ensure that the growth rate of debt is lower than the growth rate of nominal GDP, which is required to maintain a downward trajectory of the debt to GDP ratio. As a result, the PPG (Public and Publicly Guaranteed) debt to GDP ratio is expected to go below 100 percent by the end of 2025, and reach pre-pandemic levels by the end of 2028 (Figure 3).

Although a clear path to address current challenges is apparent from the fiscal side, the largest risk that needs to be addressed is the refinancing risk of the USD 500 million sukuk and the USD 100 million bond that fall due in 2026.

While USD 600 million is a significant amount to repay within a given year, especially on top of routine debt repayments (around USD300 million), arrangements are already in place to make sure that this risk does not materialize.

The plan involves two components. The first is to issue a debt instrument of USD 250 million on the international debt capital market to refinance part of the sukuk. Whether refinancing will make debt servicing more costly will depend on prevailing market conditions at the time. The strategy has the potential to generate savings too depending on global interest rates at the time. Regardless, this option dominates debt restructuring, which refers to the re-negotiation of existing debt and is effectively default.

Debt restructuring, which seems to be the proposed choice of the opposition presidential candidate, will result in the loss of investor confidence and would very likely limit our access to capital markets and private financing for a long time. The result of the latter will be economic and financial disaster, and will likely undo the progress we have achieved in building back better after the pandemic. As the cost of debt restructuring far outweighs any benefits, it is not being considered as an option and is largely unnecessary.

Secondly, the sovereign development fund (SDF), which was established specifically for the purpose of repayment foreign currency debt in challenging times, will be used to finance the remainder of the sukuk. With savings in foreign currency in the SDF resumed early this year, and an annual inflow of over MVR 1.2 billion, equivalent expected annually in the form of airport development fees.

Additionally, the foreign exchange component of cross-subsidy revenues is earmarked for the SDF. As a result, the SDF balance in foreign currency will be in excess of the required USD 250 million by 2026.

With the large bullet repayment taken care of, the USD 100 million bond and other foreign currency commitments can be serviced through the government’s tax receipts, which is estimated to reach MVR 45 billion (excluding ADF receipts which is earmarked for the SDF). Out of this, 45 percent (USD 1.5 billion) is expected to be realized in foreign currency which will be an inflow to the gross international reserves.

Despite the challenging times, the past 5 years saw the successful delivery of over 90 percent of presidential pledges and targets set in the Strategic Action Plan. The pledges for the upcoming 5 years aim to complement the development of the past five years to take the Maldives into the High-Income Country category. It is estimated that the delivery of these pledges in full will cost approximately MVR 31 billion over the next five years, which amounts to MVR 6.1 billion per annum when split equally across time.

This fiscal space will be created firstly by increasing the tax base, which the economic reforms, initiatives and developments in the manifesto will all contribute towards. Secondly, increasing the efficiency of expenditure and re-prioritization will generate further space to allocate towards the delivery of the pledges. All in all, the picture painted by the Ufaaveri Amaan Raajje manifesto demonstrates that not only can risks to fiscal and debt sustainability be managed over the medium to longer term, but that this can be achieved without foregoing the development that the Maldivian people deserve.

Note: Ibrahim Ameer is the Minister of Finance since 17 November 2018.