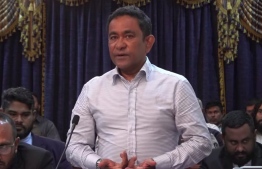

Parliament Speaker Mohamed Nasheed, on Tuesday, expressed confidence that China's commercial bank would not seize Maldivian assets, even in such an event whereby the incumbent government defaulted on the loans.

The parliament speaker and former president has long maintained his stance that Chinese loans represent a serious economic threat to Maldives, warning that China may attempt to take over the country if the government failed to settle debts.

However, in an apparent 360 turn, the speaker made the assertions otherwise, during a parliamentary session regarding possible difficulties the state may face in repaying outstanding loans and the necessity of debt restructuring.

During Tuesday's session, the parliament approved a report which called for the restructuring or reprofiling of loans excluding those sourced from foreign nations and international financial institutions.

Compiled by the Committee of the Whole House with information from the Ministry of Finance and the Maldives Monetary Authority (MMA), the report was passed with a total of 56 votes.

According to the document, loans from other nations and international organizations totaled at MVR 25.9 billion while Maldives' national debt currently stands at MVR 172 billion. Therefore, restructuring efforts are to be focused on the remaining MVR 146.1 billion of loans.

Notably, the report called for the establishment of a committee to oversee efforts to restructure Maldives national debt. The body, which will be provided technical assistance from international financial experts, must submit its findings to President Ibrahim Mohamed Solih and the parliament within an eight-month period.

The Parliamentary Committee on Public Accounts must review the debt restructuring committee's work on a monthly basis.

In order to facilitate debt restructuring, the report also urged the state to amend the Public Finance Act and the Fiscal Responsibility Act.

Furthermore, the report recommended that the Ministry of Finance rollover internal debt for 2021 and delay repayment.

In addition to the aforementioned recommendations, the parliamentary report also included several points highlighted by the committee regarding Maldives' national debt.

Despite acknowledging that the state had acquired loans at concessional rates, the report expressed concerns that sovereign bonds were sold at interest rates as high as seven percent. The report urged the state to reprofile these bonds, which must be repaid in 2022.

Overall, debts carrying sovereign guarantees were described as representing the highest risk.

The report noted that the amount allocated to settle debt was increasing year by year, with the state spending over MVR 10 billion in 2019 for loan repayment, while a figure of more than MVR 9 billion is expected in 2020.

A shortage of foreign currency was noted as a considerable risk of the increasing burden of debt repayment. The report emphasized on a need to implement measures such as reducing state expenditure in order to address the issue.

Heavily reliant on tourism for revenue, the restrictions on international travel over COVID-19 left Maldives vulnerable to severe economic repercussions. In mid-April, the World Bank projected that Maldives would be the worst-hit economy in the South Asian region due to the pandemic.

The Maldivian government estimates a shortfall of approximately USD 450 million (MVR 6.9 billion) in foreign currency and a state deficit of MVR 13 billion in 2020 as a result of the COVID-19 pandemic's impact on the tourism industry.